The call usually starts the same way. One sibling says Mom is fine because she's still driving. Another says Dad forgets more than he used to. Someone asks whether Medicare would cover help at home if things changed quickly. Then the conversation lands where families often don't want it to land: who pays, how much, and what happens if care lasts a long time.

That's the moment when long-term care planning stops being abstract.

The numbers are hard to ignore. The Federal Long Term Care Insurance Program materials show the national average annual cost of a semi-private nursing home room is about $112,420, with that figure projected to rise to nearly $186,000 in 20 years if care costs rise at an average of 2.54% annually, according to the American Association for Long-Term Care Insurance overview of long-term care need. Families who are also thinking about estate preservation often pair that insurance conversation with legal planning around shielding assets from nursing home bills, because insurance and asset protection solve different parts of the same problem.

A good long term care insurance specialist doesn't just quote a premium and wait for a signature. The right one helps a family sort through a messy real-world question: Is insurance the best tool here, or would another plan fit better?

The Conversation Every Family Eventually Has

At the kitchen table, most families aren't asking for a textbook definition of long-term care insurance. They're asking practical questions.

Can Mom stay at home if she needs help bathing or dressing? If Dad has a fall, do we have enough cash flow to cover aides, assisted living, or a facility without blowing up the rest of the retirement plan? If one child lives nearby and the others don't, who's going to manage this?

That's why the specialist matters. A seasoned long term care insurance specialist should bring structure to an emotional meeting. They should slow the conversation down, separate fear from facts, and help the family define the problem before talking about products.

What families are usually trying to protect

Sometimes the goal is preserving independence. Sometimes it's protecting a spouse who would be financially vulnerable if care expenses pile up. Sometimes the goal is simple and honest: the adult children don't want to become full-time caregivers without support.

Those are different goals, and they point to different solutions.

Practical rule: If a professional starts with a quote before asking what kind of care your family would actually want, you're not in a planning meeting. You're in a sales meeting.

A family project works better than a rushed purchase. One person can gather financial information. Another can list medications and prior diagnoses. Another can ask how each parent feels about home care, assisted living, and who they would trust to help make decisions later.

That prep turns a vague conversation into a useful one.

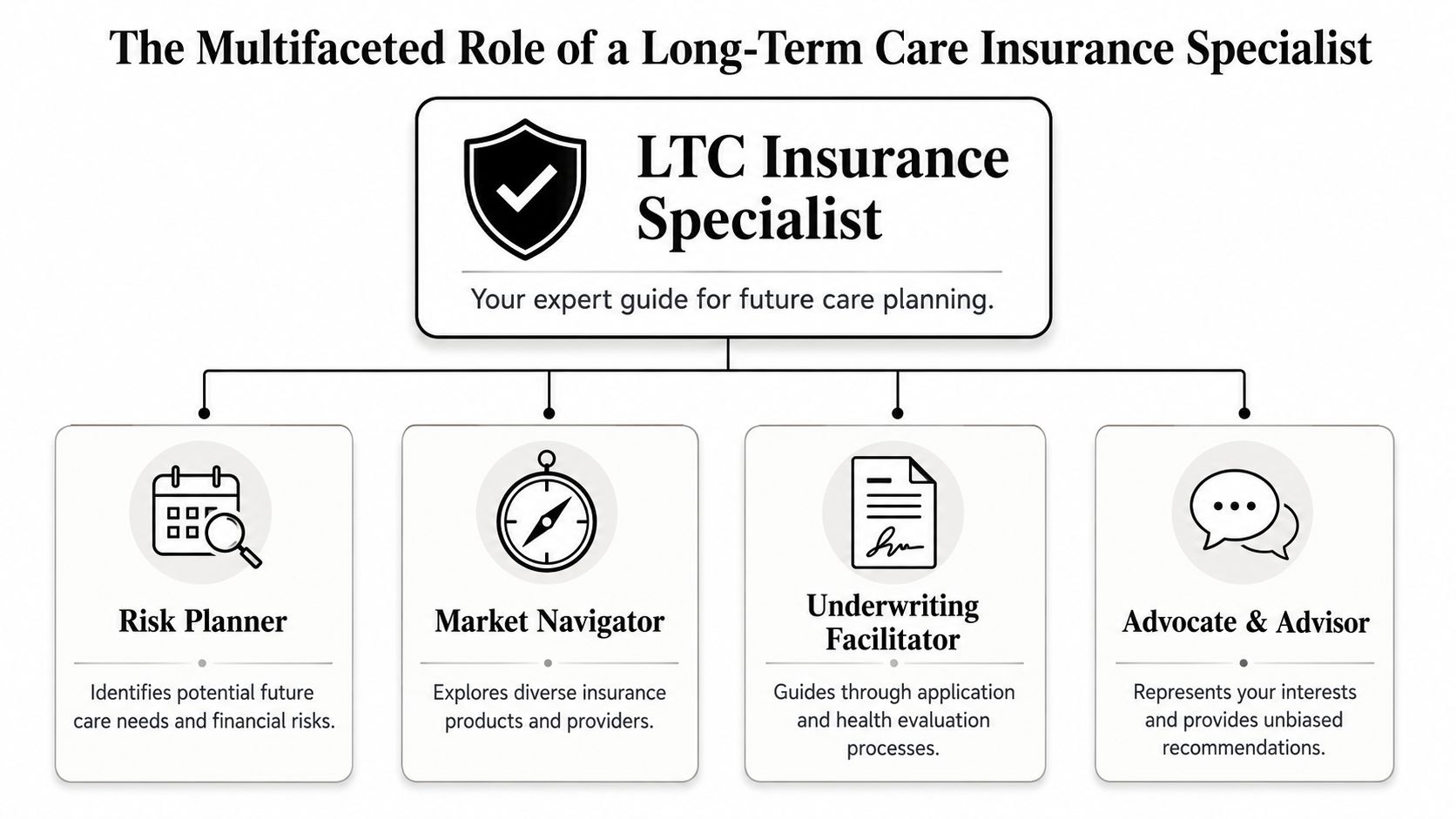

What a Long-Term Care Insurance Specialist Really Does

A long term care insurance specialist sits at the intersection of caregiving, underwriting, product design, and claims reality. That's a narrower and more practical role than what many general advisors offer.

They translate policy language into family decisions

Most families don't need more jargon. They need someone who can explain what a benefit trigger means in plain English, whether a policy supports home care in the way the family expects, and how inflation protection changes the tradeoff between lower premiums now and stronger benefits later.

If you need a plain-language refresher on core policy mechanics before meeting anyone, this overview of what long-term care insurance is is a useful starting point.

A strong specialist also knows that newer and older policies can behave very differently. Some older designs may not line up well with a family that strongly prefers care at home. That mismatch matters. Many people buy a policy thinking “coverage is coverage,” then learn later that the details drive the outcome.

They plan for underwriting, not just price

A generalist may say, “Let's see what premiums look like.” A specialist should ask different questions first.

They should ask about diagnoses, medications, mobility, prior surgeries, cognitive concerns, and family caregiving history. Not to pry, but to avoid wasting time on carriers or product types that don't fit.

The specialist's value rises because of the financial magnitude involved in long-term care. Milliman reports that annual incurred LTC insurance claims reached about $17 billion in 2024, with the average claim size growing to $180,000 in its 2024 LTC insurance statistics and experience reporting review. When claims are that large, details that look minor during shopping can become expensive mistakes later.

They should stay involved after the sale

The best specialists don't disappear once the policy is issued. They help families keep records, understand benefit triggers, and know what to do if health changes.

The measure of a good specialist isn't how fast they can get an application submitted. It's whether they help your family avoid buying the wrong coverage for the wrong reasons.

That's the core job. Risk planning, market navigation, underwriting guidance, and support when the policy is called upon.

When Your Family Should Talk to a Specialist

Most families wait too long because nobody feels sick enough, old enough, or worried enough. That delay is understandable, but it often makes planning harder.

A better approach is to treat this as a timing issue, not a crisis response. The right time to talk to a long term care insurance specialist is usually when your family can still make decisions calmly, compare options, and walk away if nothing fits.

The life moments that should trigger a meeting

You don't need a perfect age-based rule. You do need a few practical triggers.

- A parent is still healthy enough to apply. This is often the easiest planning window because choices tend to be broader and the conversation is less pressured.

- The family is updating wills, trusts, or powers of attorney. That's a natural time to ask how care would be funded.

- Someone close has a health scare or enters assisted living. Nothing sharpens the issue like seeing what care coordination really looks like.

- Adult children are starting to compare roles. If one sibling is likely to become the default helper, that affects what kind of plan makes sense.

- A parent says “I never want to be a burden.” That statement needs specifics. Does it mean preserving money, paying for home aides, or avoiding dependence on children for hands-on care?

Why families misjudge their own risk

People aren't great at estimating their own aging trajectory. A peer-reviewed study found that people often misjudge longevity, and that bias affects whether they buy long-term care insurance. The study found that those who underestimate their lifespan are less likely to buy coverage even when they have health risk factors, which is one reason objective advice matters, as detailed in this peer-reviewed analysis of LTC insurance demand and survival beliefs.

That finding lines up with what families do in real life. One parent says, “I won't live that long anyway.” Another says, “If something happens, you kids will figure it out.” Both statements may feel comforting in the moment. Neither is a plan.

Here's a useful primer to watch before a family meeting if you want a broad overview of the topic.

What an objective third party changes

A specialist can put real scenarios on the table without the family sounding alarmist. That matters.

For example, they can ask, “If care starts at home and lasts longer than expected, do you want to pay from income, from investments, from a dedicated policy, or some combination?” That question is more productive than “Do you think you'll ever need care?”

How to Locate and Vet Potential Specialists

Finding candidates isn't the hard part. Filtering them is.

Families get into trouble when they confuse access with expertise. Plenty of professionals can offer a long-term care insurance quote. Fewer can explain carrier differences clearly, discuss rate stability accurately, and tell you when a recommendation doesn't fit your budget or health profile.

Where to start looking

Referrals from estate planning attorneys, elder law attorneys, and financial professionals can be useful if those referrals come with context. Ask why they recommend that person. “She's responsive” isn't enough. “He's good at pre-screening health issues and explaining policy structure” is better.

It also helps to review broader criteria for interviewing financial professionals. This guide to selecting an advisor isn't specific to long-term care, but its framing around process, conflicts, and fit is useful when you're comparing specialists.

If cost and public benefits are part of your family discussion, it's also smart to understand what public guidance is available through programs like the State Health Insurance Assistance Program. That won't replace specialist advice, but it can sharpen your questions.

What to listen for in the first call

A real specialist should spend meaningful time asking about your family before talking about products. They should ask whether the goal is home care, asset protection, relieving children of caregiving pressure, or preserving flexibility. They should also ask enough health questions to determine whether a traditional policy is realistic before sending everyone down the wrong path.

The second thing to test is whether they can discuss premium durability without getting slippery. New York's insurance regulator explains that rate applications require detailed actuarial support, and consumer reporting notes that some policyholders have seen increases over 80%, which is why New York's methodology for reviewing LTC rate applications is so relevant to buyer vetting.

What works: “Here's how I stress-test affordability if premiums rise later, and here are the policy features we can adjust.”

What doesn't: “Let's just focus on today's price.”

Interview Checklist for a Long-Term Care Insurance Specialist

| Question Category | Specific Question to Ask |

|---|---|

| Background | How much of your work is specifically long-term care planning versus general insurance or retirement products? |

| Process | What information do you gather before showing any quotes? |

| Health screening | How do you pre-screen likely underwriting issues before applying? |

| Carrier comparison | Which policy features do you compare besides premium, especially home care coverage and benefit triggers? |

| Rate stability | How do you evaluate an insurer's history of rate increases and discuss future affordability? |

| Stress testing | How will you show us what happens if premiums rise later and we need a lower-cost fallback? |

| Alternatives | In what situations do you tell a family not to buy a traditional policy? |

| Outdated coverage | How do you identify when an older policy design is a poor fit for current caregiving goals? |

| Family fit | How do you help siblings or spouses compare insurance against keeping assets liquid? |

| Claims support | If we buy, what help do you provide later when it's time to use benefits? |

Green flags and red flags

A green flag is specificity. The specialist can explain why one policy might fit a home-care-first family better than another. They can talk about tradeoffs without pushing you to a quick yes.

A red flag is impatience with hard questions. If you ask about premium sustainability, reduced-benefit options, or what happens if you never use the policy, and the answer feels evasive, move on.

Preparing for Your Consultation

A consultation goes better when the family treats it as a working session, not a lecture. That means gathering facts, naming goals, and deciding in advance who's speaking for whom.

If you show up with no health summary, no sense of budget, and no agreement about what problem you're trying to solve, the meeting will drift toward generic recommendations.

What to bring

The paperwork doesn't need to be fancy. A one-page summary is often enough to make the meeting far more productive.

- Basic financial picture: List income sources, major assets, and any concerns about protecting a surviving spouse or preserving funds for future care.

- Health snapshot: Include diagnoses, medications, recent surgeries, mobility concerns, and any memory or cognitive changes that have already surfaced.

- Current coverage: Bring existing life insurance, annuity, disability, or long-term care policies if anyone already owns them.

- Family history notes: Not because it predicts everything, but because it helps frame how the family thinks about aging, dementia, and long care periods.

- Care preferences: Write down whether staying at home matters most, whether assisted living is acceptable, and who would likely coordinate care if a crisis happened.

What to decide before the meeting

Families often think they need to agree on everything first. They don't. They do need to identify the biggest tensions.

Maybe one sibling wants maximum protection and another worries about locking up cash in premiums. Maybe a parent wants to leave money to heirs, while the children care more about paying for support that reduces family burnout. Those tensions are normal.

Bring disagreements into the room early. A skilled specialist can work with conflict that's visible. Hidden conflict usually resurfaces after the recommendation, when trust is lower and the decision feels more personal.

Turn the consultation into a two-way interview

Ask the specialist to explain their reasoning, not just their conclusion.

For example, if they recommend a traditional policy, ask what family scenario that policy solves best. If they lean against coverage, ask whether the issue is budget, underwriting fit, policy design, or a better alternative. If they mention reducing benefits to keep premiums manageable, ask what protection you'd be giving up in practice.

That's how you keep the meeting grounded. You're not there to be impressed. You're there to make a difficult choice with fewer blind spots.

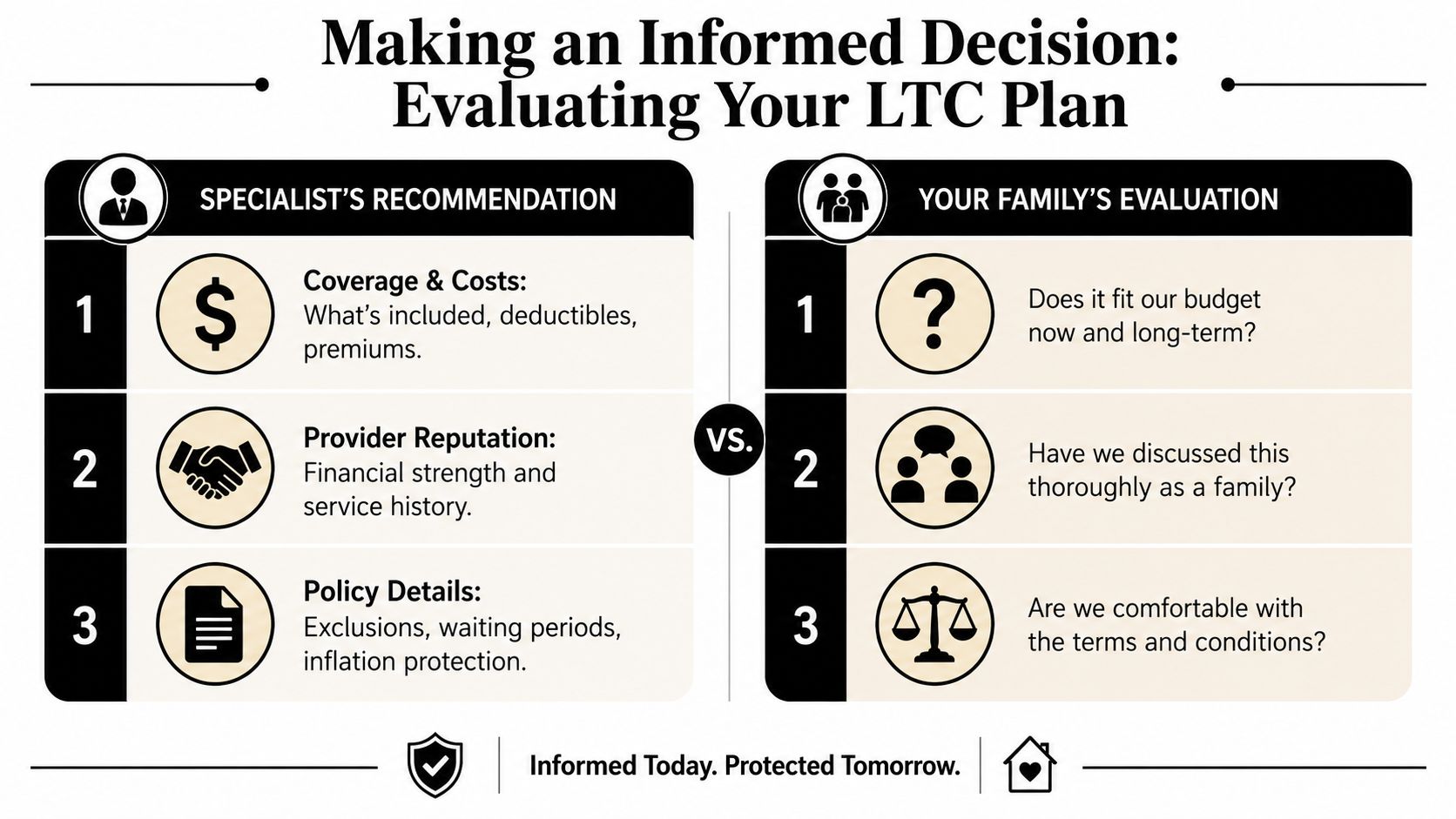

Evaluating the Recommendation and Next Steps

The specialist's recommendation is the start of the decision, not the end of it.

Families should pressure-test any recommendation against one simple question: Are we solving the right problem, in a way we can live with over time? That means evaluating the product, the premium, the likely usefulness, and the opportunity cost of not keeping that money liquid.

The decision test that matters most

One of the most important family tradeoffs is whether to pay ongoing premiums or keep assets available for caregiving, housing changes, and future flexibility. That tradeoff is central because most care is still paid out of pocket or through Medicaid after assets are depleted, as discussed in this explanation of what a long-term care insurance specialist should help families compare.

That means “Is this worth it?” is the right question.

Sometimes the answer is yes. A policy may protect a spouse, support home care preferences, and move a meaningful chunk of risk off the family balance sheet. Sometimes the answer is no. The premiums may strain retirement income, the underwriting may not cooperate, or the family may reasonably prefer another strategy.

If the best answer is not to buy

That outcome is more common than many families expect, and it's not a failure.

A thoughtful plan might involve self-funding from assets, using a hybrid life and long-term care approach, relying on other investments, or preparing for future use of public programs after private resources are spent down. Some families also need a non-insurance care plan first, especially if the bigger issue is family coordination rather than financial transfer.

If you're comparing insurance with the broader menu of care settings and support options, it helps to understand the range of long-term care services your family may use.

How to know you're ready to decide

You're ready when the family can answer these questions clearly:

- Budget fit: Can we afford this now without resentment later?

- Use-case fit: Does this match where and how we'd want care delivered?

- Fallback plan: If the recommendation doesn't work out, what's Plan B?

- Family buy-in: Have the key decision-makers heard the same explanation and reacted to the same numbers?

- Emotional fit: Will this choice reduce stress for the people who would carry the burden if care is needed?

A good long term care insurance specialist earns trust by making it easier to say no when no is the right answer.

That's the standard families should use.

If you're trying to turn a complicated family discussion into a practical action plan, Family Caregiving Kit offers clear guides, tools, and decision aids that help relatives gather information, compare options, and move from vague worry to manageable next steps.